Feature Selection

This page was created from a Jupyter notebook. The original notebook can be found here. It investigates which attributes in the database to select for further study. First we must import the necessary installed modules.

import matplotlib.pyplot as plt

import seaborn as sns

from functools import partial

from sklearn.preprocessing import LabelEncoder, FunctionTransformer, MinMaxScaler

from sklearn.feature_selection import SelectKBest, chi2, f_classif

from sklearn.pipeline import make_pipeline

from sklearn.linear_model import LogisticRegression

import datetime as dt

import matplotlib.dates as mdates

Next we need to import a few local modules.

import os

import sys

module_path = os.path.abspath(os.path.join('..'))

if module_path not in sys.path:

sys.path.append(module_path)

from databall.database import Database

from databall.model_selection import train_test_split

from databall.plotting import cross_val_curves, format_538

from databall.plotting import cross_val_precision_recall_curve, cross_val_roc_curve

from databall.profit import profit

from databall.simulate import simulate

from databall.util import select_columns, stat_names

As before, let’s apply the FiveThirtyEight plot style.

plt.style.use('fivethirtyeight')

Collect the Data

The first step is to bring in the data similar to what was done during data exploration.

database = Database('../data/nba.db')

The betting stats method combines game stats with betting data. The method takes a rolling average of stats where the window size (number of games to average over) is determined by the window parameter. The beginning of the season where the rolling window is invalid is filled in with an expanding mean. I removed all seasons prior to 2006 to reduce the computational time of cross-validation and parameter tuning efforts.

games = database.betting_stats(window=10)

games = games[games.SEASON>=2006]

Straight Up vs. Spread Betting

First let’s look at how well we do if we simply bet on the favorite. The code below creates a pandas DataFrame that always predicts the favorite (indicated by a negative point spread) wins. The profit function looks at the predicted variable and calculates the profit at the end of each day of the season.

predictions = games.loc[games.SEASON==2016, ['SEASON', 'GAME_DATE', 'TEAM_NET_RTG', 'TEAM_NET_RTG_AWAY',

'HOME_SPREAD', 'HOME_WL', 'HOME_SPREAD_WL']].dropna()

predictions['HOME_WL_PRED'] = 'W'

predictions['HOME_SPREAD_WL_PRED'] = 'W'

predictions.loc[predictions.HOME_SPREAD > 0, ['HOME_WL_PRED', 'HOME_SPREAD_WL_PRED']] = 'L'

var_predict = 'HOME_SPREAD_WL'

days, cumper, cumprofit = profit(predictions, var_predict='HOME_WL', bet_amount=100)

days_spread, cumper_spread, cumprofit_spread = profit(predictions, var_predict=var_predict, bet_amount=100)

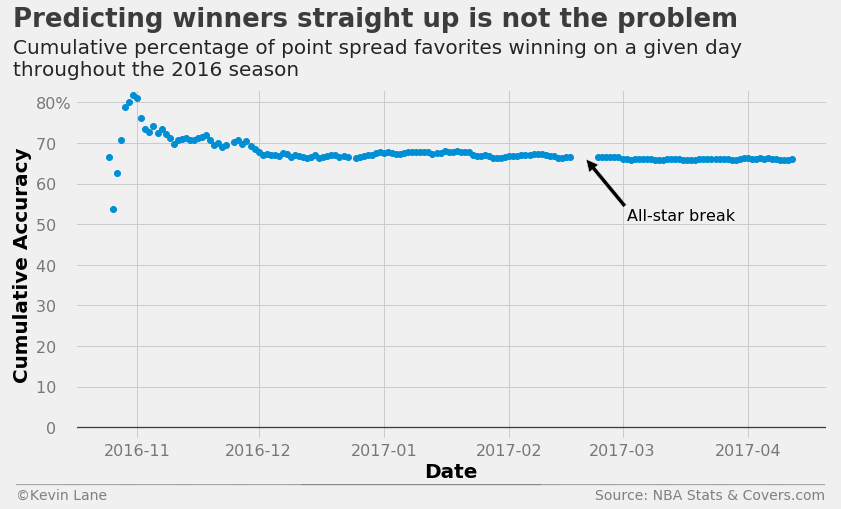

The chart below tracks cumulative accuracy of betting on the favorite to win straight up. This uses no machine learning at all and simply says the home team wins if the home point spread is negative. This works quite well for predicting winners straight up and settles out to almost 70% accuracy.

fig = plt.figure(figsize=(12, 6))

plt.plot_date(days, cumper*100)

plt.ylim(-3)

x = [dt.datetime(2017, 2, 20), dt.datetime(2017, 3, 2)]

plt.annotate('All-star break', xy=(mdates.date2num(x[0]),66), xytext=(mdates.date2num(x[1]),51),

fontsize=16, arrowprops=dict(facecolor='black'))

title = 'Predicting winners straight up is not the problem'

subtitle = '''Cumulative percentage of point spread favorites winning on a given day

throughout the 2016 season'''

format_538(fig, 'NBA Stats & Covers.com', xlabel='Date', ylabel='Cumulative Accuracy', title=title,

subtitle=subtitle, xoff=(-0.09, 1.01), yoff=(-0.12, -0.17), toff=(-0.082, 1.18),

soff=(-0.082, 1.04), suffix='%', suffix_offset=3)

plt.show()

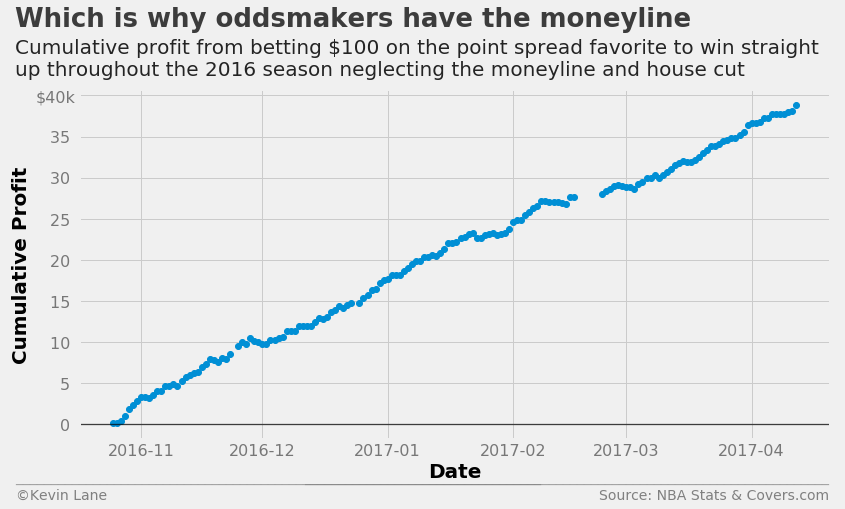

The chart below shows cumulative profit in a hypothetical scenario where bettors are allowed to bet on winners straight up with no moneyline or house cut. It is absurdly profitable, which is why oddsmakers have the moneyline in the first place. When betting on favorites straight up, bettors must risk more money than they win according to the moneyline. I was unable to find historical moneyline numbers, so that aspect is neglected.

fig = plt.figure(figsize=(12, 6))

plt.plot_date(days, cumprofit/1000)

title = 'Which is why oddsmakers have the moneyline'

subtitle = '''Cumulative profit from betting $100 on the point spread favorite to win straight

up throughout the 2016 season neglecting the moneyline and house cut'''

format_538(fig, 'NBA Stats & Covers.com', xlabel='Date', ylabel='Cumulative Profit', title=title,

subtitle=subtitle, xoff=(-0.095, 1.01), yoff=(-0.12, -0.17), toff=(-0.085, 1.18),

soff=(-0.085, 1.04), prefix='$', suffix='k', suffix_offset=1)

plt.show()

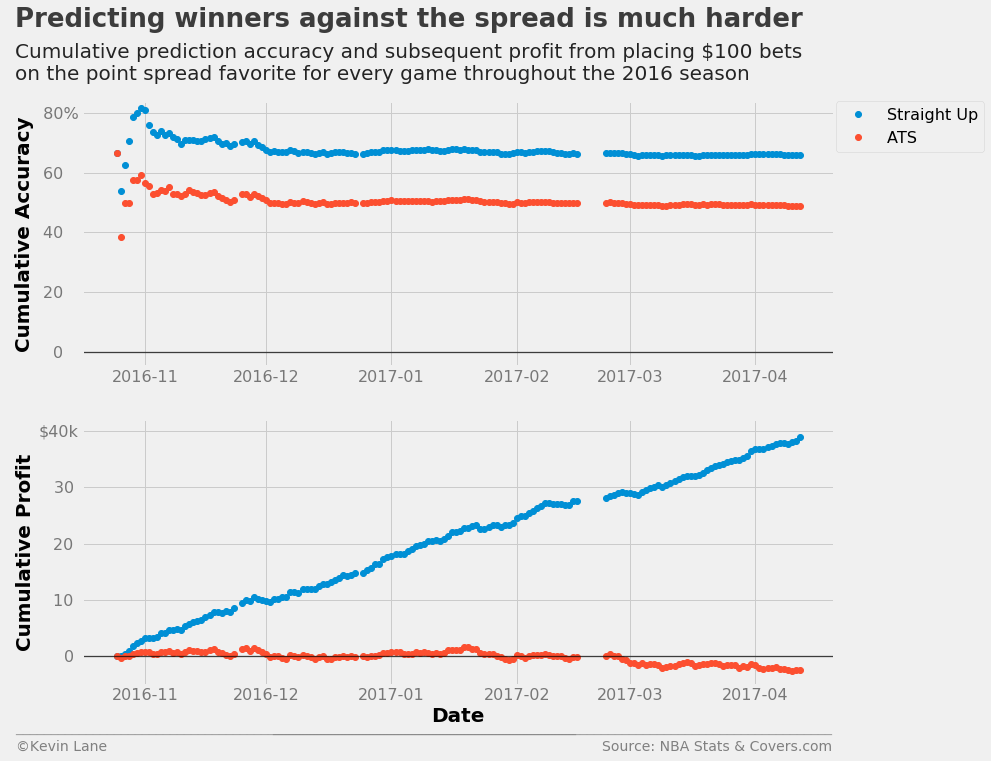

Following the same procedure for predicting winners against the spread is not as successful. The accuracy settles out to a hair below 50% and we end up losing a little bit of money. This accuracy makes sense since we saw during data exploration that home teams win about 50% of the time against the spread.

fig = plt.figure(figsize=(12, 10))

ax1 = plt.subplot(211)

ax1.plot_date(days, cumper*100, label='Straight Up')

ax1.plot_date(days_spread, cumper_spread*100, label='ATS')

ax1.set_ylabel('Cumulative Accuracy')

ax1.set_ylim(-5)

ax1.legend(fontsize=16, bbox_to_anchor=(1.2, 1), borderaxespad=0)

ax2 = plt.subplot(212)

ax2.plot_date(days, cumprofit/1000, label='Straight Up')

ax2.plot_date(days_spread, cumprofit_spread/1000, label='ATS')

ax2.set_xlabel('Date')

ax2.set_ylabel('Cumulative Profit')

ax2.set_ylim(-5, 42)

title = 'Predicting winners against the spread is much harder'

subtitle = '''Cumulative prediction accuracy and subsequent profit from placing $100 bets

on the point spread favorite for every game throughout the 2016 season'''

format_538(fig, 'NBA Stats & Covers.com', ax=(ax1, ax2), title=title, subtitle=subtitle,

xoff=(-0.1, 1.01), yoff=(-1.38, -1.45), toff=(-.09, 1.28), soff=(-0.09, 1.08),

prefix = (' ', '$'), suffix=('%', 'k'), suffix_offset=(3, 1), n=80)

plt.show()

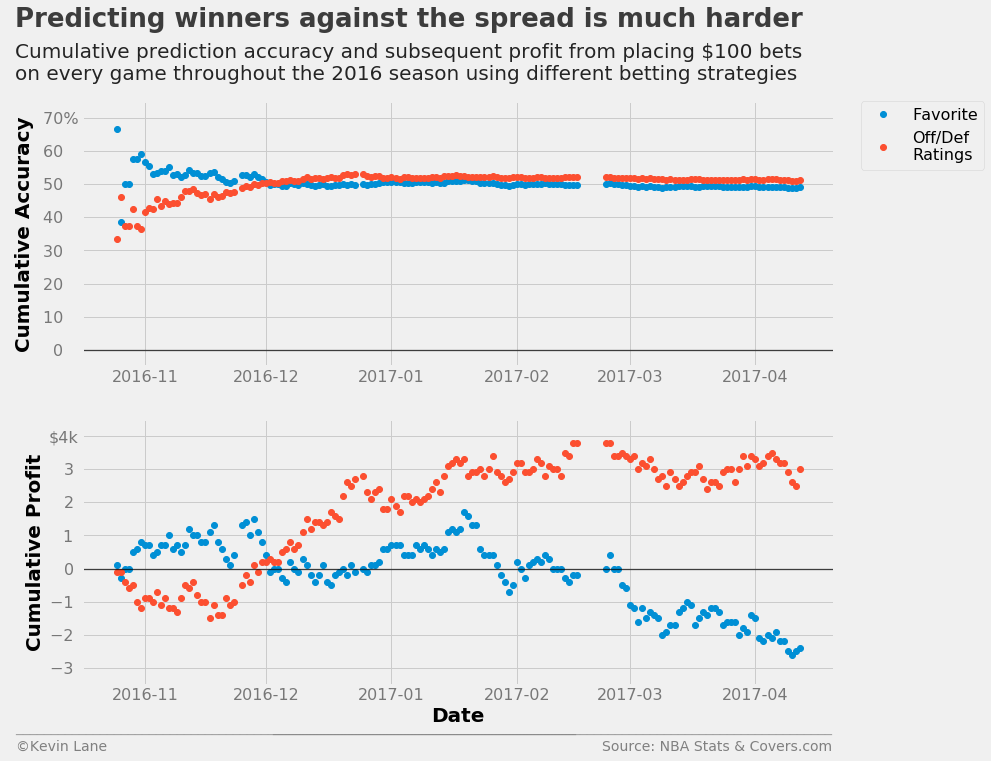

Offensive/Defensive Ratings

As a first attempt at predicting game winners against the spread using machine learning, I used logistic regression trained with home point spread and offensive and defensive ratings. Logistic regression (using scikit-learn’s LogisticRegression class) is well-suited to this type of binary classification problem and when trained with team point ratings was the best-performing model in the initial project for predicting home winners straight up, so it was a reasonable place to start. The simulate method makes predictions on each day of the season and allows retraining with games already predicted. Retraining is explored in model performance. The predicted variable encodes the W/L values to 1 and 0 using scikit-learn’s LabelEncoder class.

ratings = ['TEAM_OFF_RTG', 'TEAM_DEF_RTG', 'TEAM_OFF_RTG_AWAY', 'TEAM_DEF_RTG_AWAY', 'HOME_SPREAD']

games_sub = games[ratings + ['SEASON', 'GAME_DATE', var_predict]].dropna()

output = simulate(LogisticRegression(), games_sub, 2016, ratings, var_predict)

days_rtg, cumper_rtg, cumprofit_rtg = profit(output, var_predict=var_predict, bet_amount=100)

This method starts out worse than just betting on the favorite, but eventually overtakes it about a month into the season and ends up making about $3,000. While the model results in a profit, the return on investment is very low. This assumes bettors make $100 bets on every game, which results in a total of $123,000 wagered at the end of a full-length season (82 games in a 30-team league).

fig = plt.figure(figsize=(12, 10))

ax1 = plt.subplot(211)

ax1.plot_date(days_spread, cumper_spread*100, label='Favorite')

ax1.plot_date(days_rtg, cumper_rtg*100, label='Off/Def\nRatings')

ax1.set_ylabel('Cumulative Accuracy')

ax1.set_ylim(-5, 75)

ax1.legend(fontsize=16, bbox_to_anchor=(1.2, 1), borderaxespad=0)

ax2 = plt.subplot(212)

ax2.plot_date(days_spread, cumprofit_spread/1000)

ax2.plot_date(days_rtg, cumprofit_rtg/1000)

ax2.set_xlabel('Date')

ax2.set_ylabel('Cumulative Profit')

ax2.set_ylim(-3.5, 4.5)

title = 'Predicting winners against the spread is much harder'

subtitle = '''Cumulative prediction accuracy and subsequent profit from placing $100 bets

on every game throughout the 2016 season using different betting strategies'''

format_538(fig, 'NBA Stats & Covers.com', ax=(ax1, ax2), title=title, subtitle=subtitle,

xoff=(-0.1, 1.01), yoff=(-1.38, -1.45), toff=(-.09, 1.28), soff=(-0.09, 1.08),

prefix = (' ', '$'), suffix=('%', 'k'), suffix_offset=(3, 1), n=80)

plt.show()

Next I wanted to look at some cross-validation. The function below grabs all seasons between 2006-2016 and reserves the 2016 season as the test set.

x_train, y_train, x_test, y_test = train_test_split(games, 2006, 2016, ylabel=var_predict,

xlabels=stat_names() + ['SEASON', 'HOME_WL'])

x_train = x_train.drop('SEASON', axis=1)

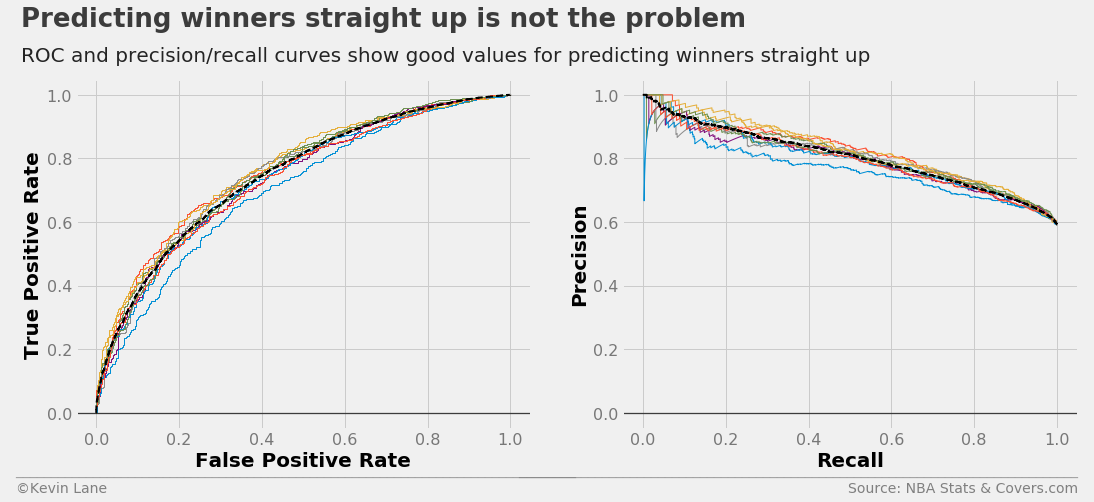

The code below plots cross-validated ROC and precision/recall curves. It also plots the curves for each fold of the cross validation. It first performs a k-fold cross-validation to get the predicted probabilities of each instance using cross_val_predict and StratifiedKFold. The predicted probabilities of the positive class (home team wins) are input into roc_curve and roc_auc_score to get the mean ROC curve and area under the curve. The process is similar for the cross-validated precision/recall curve using precision_recall_curve and average_precision_score. The areas under the curves are displayed on the legend when the legend is shown.

season = 2016

y = LabelEncoder().fit_transform(x_train.HOME_WL)

model = LogisticRegression()

fig, ax1, ax2 = cross_val_curves(model, x_train[ratings], y, legend=False)

title = 'Predicting winners straight up is not the problem'

subtitle = 'ROC and precision/recall curves show good values for predicting winners straight up'

format_538(fig, 'NBA Stats & Covers.com', ax=(ax1, ax2), title=title, subtitle=subtitle,

xoff=(-0.15, 2.22), yoff=(-0.13, -0.18), toff=(-.12, 1.15), soff=(-0.12, 1.05), n=80)

plt.show()

An ROC curve compares a classifier’s true positive rate (\(TPR\)) to its false positive rate (\(FPR\)), where:

\[\begin{align} TPR & =\frac{TP}{TP+FN} \\ FPR & =\frac{FP}{FP+TN} \\ TP & =\text{true positive} \\ FP & =\text{false positive} \\ TN & =\text{true negative} \\ FN & =\text{false negative} \end{align}\]Therefore, a perfect classifier (\(TPR=1\) and \(FPR=0\)) would be located in the upper left corner of an ROC curve. The aptly-named precision/recall curve compares a classifier’s precision with its recall, which are defined as:

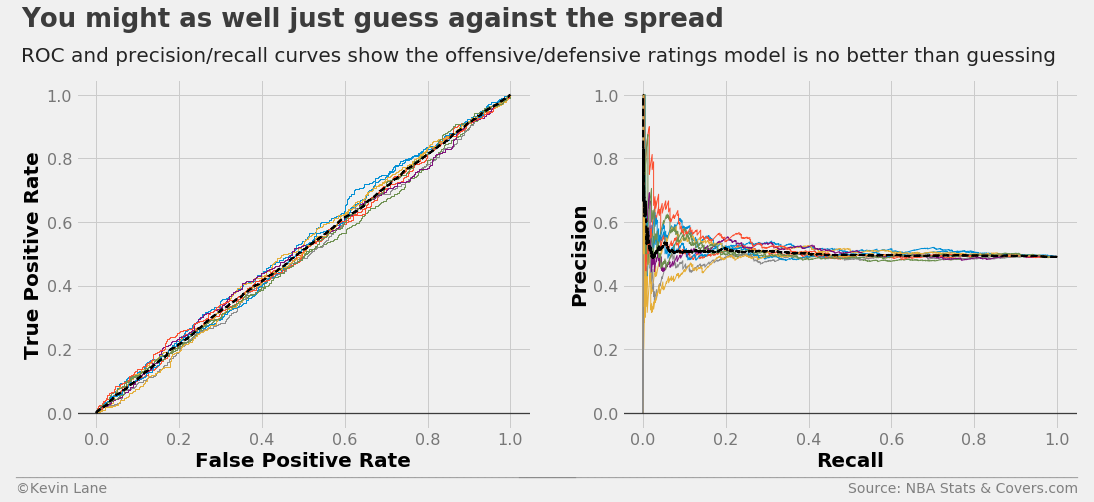

\[\begin{align} \text{Precision} & =\frac{TP}{TP+FP} \\ \text{Recall} & =TPR \end{align}\]making the ideal point of a precision/recall curve the upper right corner. The ROC and precision/recall curves below are for winners against the spread. The nearly y=x relationship of the ROC curve and flat precision/recall curve indicate the model is no better than random guessing, which makes sense given it is about 50% accurate.

model = LogisticRegression()

fig, ax1, ax2 = cross_val_curves(model, x_train[ratings], y_train, legend=False)

title = 'You might as well just guess against the spread'

subtitle = 'ROC and precision/recall curves show the offensive/defensive ratings model is no better than guessing'

format_538(fig, 'NBA Stats & Covers.com', ax=(ax1, ax2), title=title, subtitle=subtitle,

xoff=(-0.15, 2.22), yoff=(-0.13, -0.18), toff=(-.12, 1.15), soff=(-0.12, 1.05), n=80)

plt.show()

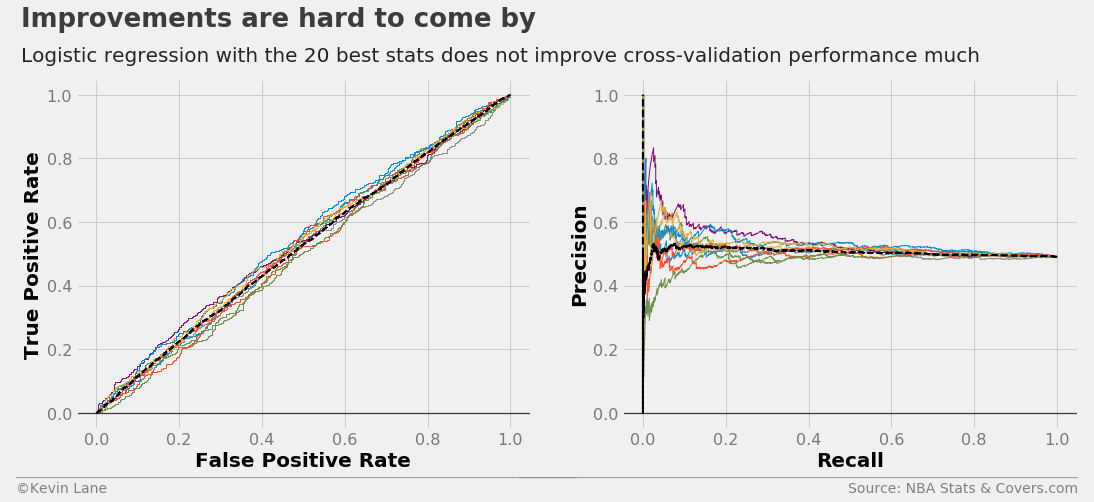

Select Features Automatically

Next I wanted to investigate how well automatically-selected stats perform. The code below uses SelectKBest to select the 20 best attributes according to the ANOVA F-value. This uses a process called univariate feature selection, which uses univariate statistical tests to select features. In the first project, the majority of automatically-selected attributes were point ratings (SRS, offensive rating, etc.). However none of the point rating stats appear until well down the list. The FOUR_FACTORS stat is the weighted sum of the four factors. The FOUR_FACTORS_REB stat is identical with the exception that it includes defensive rebounds. The two definitions of the four factors are weighted according to Oliver’s selected weights (discussed during stat collection) and combined into single metrics as:

\(FF=0.4*EFG\% + 0.2*OREB\% + 0.15*FTR - 0.25*TOV\%\) \(FF_{REB}=0.4*EFG\% + 0.1*OREB\% + 0.1*DREB\% + 0.15*FTR - 0.25*TOV\%\)

if 'HOME_WL' in x_train.columns:

x_train = x_train.drop('HOME_WL', axis=1)

kbest_anova = SelectKBest(f_classif, k=20).fit(x_train, y_train)

for label in x_train.columns[kbest_anova.get_support()]:

print(label)

TEAM_FG3M

TEAM_FG3A

TEAM_STL

OPP_FG3M

OPP_OREB

OPP_AST

TEAM_FGM_AWAY

TEAM_FGA_AWAY

TEAM_DREB_AWAY

TEAM_REB_AWAY

OPP_FGA_AWAY

OPP_FG3A_AWAY

TEAM_OFF_RTG

TEAM_FOUR_FACTORS

TEAM_FOUR_FACTORS_REB

TEAM_OFF_RTG_AWAY

TEAM_NET_RTG_AWAY

TEAM_FOUR_FACTORS_AWAY

TEAM_FOUR_FACTORS_REB_AWAY

POSSESSIONS_AWAY

Selecting the 20 best features using a chi-square test selects similar attributes as the ANOVA F-value above. The chi-square test only works on positive values, so each feature in the training data is scaled to fall between 0 and 1 using the MinMaxScaler class.

kbest_chi2 = SelectKBest(chi2, k=20).fit(MinMaxScaler((0, 1)).fit_transform(x_train), y_train)

for label in x_train.columns[kbest_chi2.get_support()]:

print(label)

TEAM_FG3M

TEAM_FG3A

TEAM_STL

OPP_FG3M

OPP_AST

TEAM_FGM_AWAY

TEAM_FGA_AWAY

TEAM_FG3A_AWAY

TEAM_FTA_AWAY

TEAM_DREB_AWAY

TEAM_REB_AWAY

OPP_FGA_AWAY

OPP_FG3A_AWAY

OPP_AST_AWAY

TEAM_FOUR_FACTORS_REB

TEAM_OFF_RTG_AWAY

TEAM_NET_RTG_AWAY

TEAM_FOUR_FACTORS_AWAY

TEAM_FOUR_FACTORS_REB_AWAY

POSSESSIONS_AWAY

The ROC and precision/recall curves below use the 20 best stats selected by the ANOVA F-value. They appear very similar to those about using offensive/defensive ratings.

kbest_stats = x_train.columns[kbest_anova.get_support()].tolist()

model = LogisticRegression()

fig, ax1, ax2 = cross_val_curves(model, x_train[kbest_stats], y_train, legend=False)

title = 'Improvements are hard to come by'

subtitle = 'Logistic regression with the 20 best stats does not improve cross-validation performance much'

format_538(fig, 'NBA Stats & Covers.com', ax=(ax1, ax2), title=title, subtitle=subtitle,

xoff=(-0.15, 2.22), yoff=(-0.13, -0.18), toff=(-.12, 1.15), soff=(-0.12, 1.05), n=80)

plt.show()

The code below calculates profit for the 2016 season using the 20 best stats for a comparison at the end.

games_sub = games[kbest_stats + ['SEASON', 'GAME_DATE', var_predict]].dropna()

output = simulate(LogisticRegression(), games_sub, 2016, kbest_stats, var_predict)

days_kbest, cumper_kbest, cumprofit_kbest = profit(output, var_predict=var_predict, bet_amount=100)

Compare Attribute Groupings

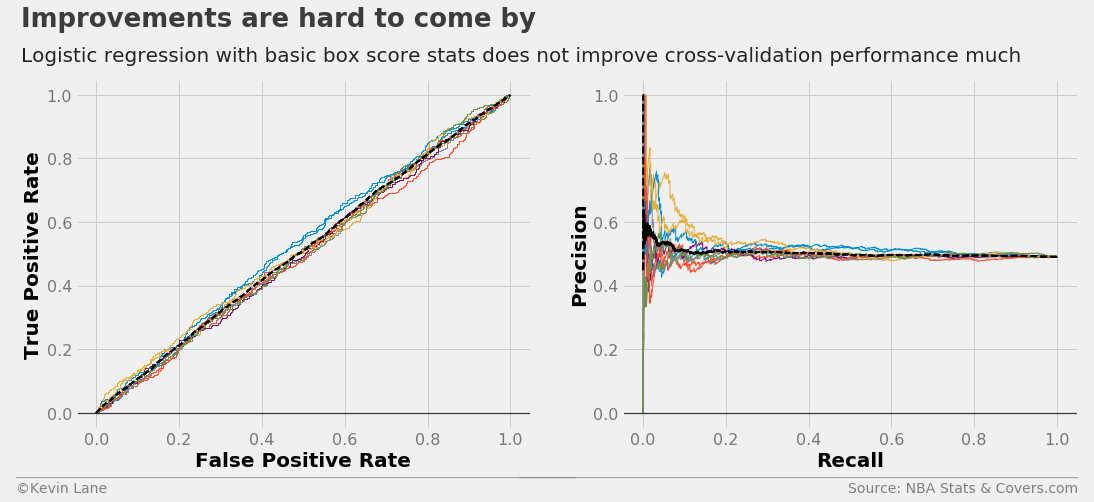

I then wanted to test a simpler method using only basic box score stats (FG, REB, AST, etc.) for the average user. The ROC and precision/recall curves below do not show much improvement.

stats = ['FGM', 'FGA', 'FG3M', 'FG3A', 'FTM', 'FTA', 'OREB', 'DREB', 'REB', 'AST', 'TOV', 'STL', 'BLK']

stats = ['TEAM_' + s for s in stats] + ['POSSESSIONS']

stats += [s + '_AWAY' for s in stats] + ['HOME_SPREAD']

model = LogisticRegression()

fig, ax1, ax2 = cross_val_curves(model, x_train[stats], y_train, legend=False)

title = 'Improvements are hard to come by'

subtitle = 'Logistic regression with basic box score stats does not improve cross-validation performance much'

format_538(fig, 'NBA Stats & Covers.com', ax=(ax1, ax2), title=title, subtitle=subtitle,

xoff=(-0.15, 2.22), yoff=(-0.13, -0.18), toff=(-.12, 1.15), soff=(-0.12, 1.05), n=80)

plt.show()

The code below calculates profit for the 2016 season using basic box score stats for a comparison at the end.

games_sub = games[stats + ['SEASON', 'GAME_DATE', var_predict]].dropna()

output = simulate(LogisticRegression(), games_sub, 2016, stats, var_predict)

days_box, cumper_box, cumprofit_box = profit(output, var_predict=var_predict, bet_amount=100)

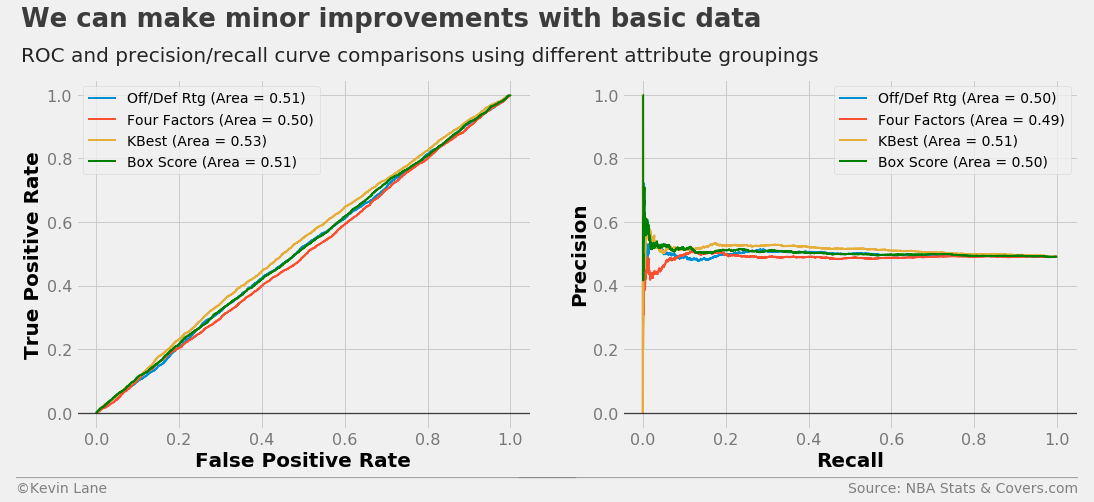

The code below plots 10-fold cross-validated ROC and precision/recall curves using logistic regression models trained with different attribute groupings. I added a FunctionTransformer that selects columns from the DataFrame to simplify the process of specifying all the attributes. The selector and classifier are combined into a scikit-learn Pipeline using the make_pipeline function.

# Define attributes to use for each curve

four_factors = ['EFG', 'TOV_PCT', 'OREB_PCT', 'DREB_PCT', 'FT_PER_FGA']

attributes = [['OFF_RTG', 'DEF_RTG'], four_factors, kbest_stats, stats]

labels = ['Off/Def Rtg', 'Four Factors', 'KBest', 'Box Score']

fig = plt.figure(figsize=(16, 6))

ax1 = plt.subplot(121)

# Plot ROC curves for each set of attributes

for (a, l) in zip(attributes, labels):

# Make transformer that selects the desired attributes from the DataFrame

selector = FunctionTransformer(partial(select_columns, attributes=a, columns=x_train.columns))

# Make a pipeline that selects the desired attributes prior to the classifier

model = make_pipeline(selector, LogisticRegression())

cross_val_roc_curve(model, x_train, y_train, ax1, label=l, show_folds=False)

ax1.get_lines()[-1].set_color('green')

ax1.legend(fontsize=14)

ax2 = plt.subplot(122)

# Plot ROC curves for each set of attributes

for (a, l) in zip(attributes, labels):

# Make transformer that selects the desired attributes from the DataFrame

selector = FunctionTransformer(partial(select_columns, attributes=a, columns=x_train.columns))

# Make a pipeline that selects the desired attributes prior to the classifier

model = make_pipeline(selector, LogisticRegression())

cross_val_precision_recall_curve(model, x_train, y_train, ax2, label=l, show_folds=False)

ax2.get_lines()[-1].set_color('green')

ax2.legend(fontsize=14)

title = 'We can make minor improvements with basic data'

subtitle = 'ROC and precision/recall curve comparisons using different attribute groupings'

format_538(fig, 'NBA Stats & Covers.com', ax=(ax1, ax2), title=title, subtitle=subtitle,

xoff=(-0.15, 2.22), yoff=(-0.13, -0.18), toff=(-.12, 1.15), soff=(-0.12, 1.05), n=80)

plt.show()

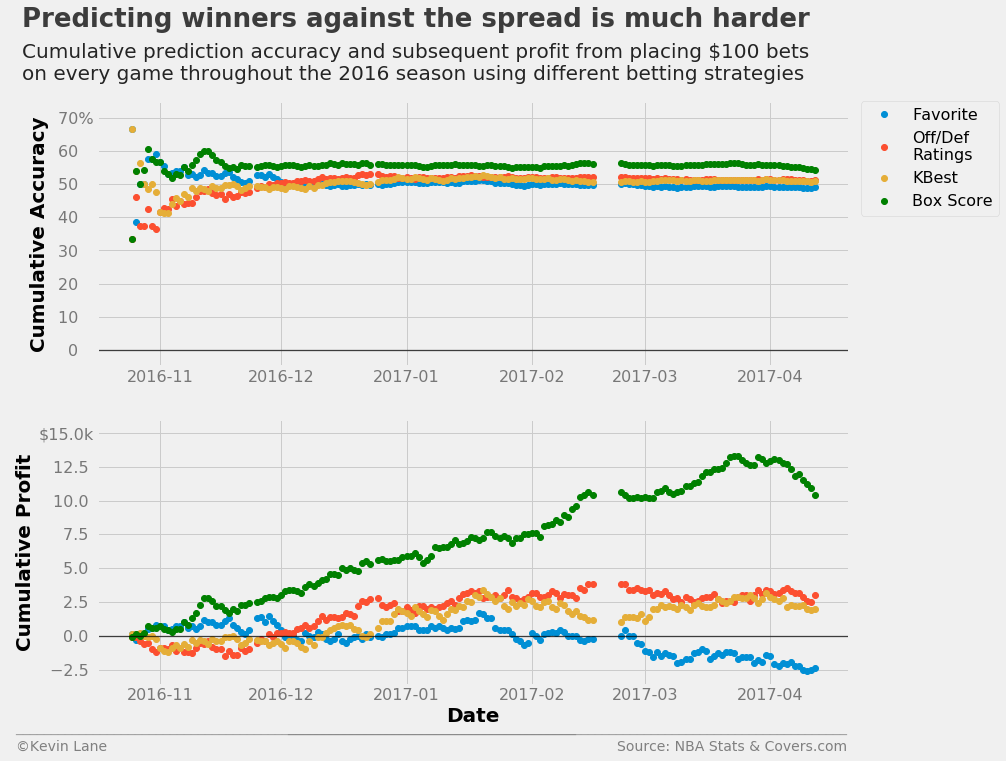

The plots below show accuracy and profits throughout the 2016 season using logistic regression models trained with different sets of stats compared with simply picking the favorite. All the logistic regression models end up making money, but the model trained with the complete set of box score stats outperforms all others.

fig = plt.figure(figsize=(12, 10))

ax1 = plt.subplot(211)

ax1.plot_date(days_spread, cumper_spread*100, label='Favorite')

ax1.plot_date(days_rtg, cumper_rtg*100, label='Off/Def\nRatings')

ax1.plot_date(days_kbest, cumper_kbest*100, label='KBest')

ax1.plot_date(days_box, cumper_box*100, label='Box Score', color='green')

ax1.set_ylabel('Cumulative Accuracy')

ax1.set_ylim(-5, 75)

ax1.legend(fontsize=16, bbox_to_anchor=(1.2, 1), borderaxespad=0)

ax2 = plt.subplot(212)

ax2.plot_date(days_spread, cumprofit_spread/1000)

ax2.plot_date(days_rtg, cumprofit_rtg/1000)

ax2.plot_date(days_kbest, cumprofit_kbest/1000)

ax2.plot_date(days_box, cumprofit_box/1000, color='green')

ax2.set_xlabel('Date')

ax2.set_ylabel('Cumulative Profit')

ax2.set_ylim(-3.6, 16)

title = 'Predicting winners against the spread is much harder'

subtitle = '''Cumulative prediction accuracy and subsequent profit from placing $100 bets

on every game throughout the 2016 season using different betting strategies'''

format_538(fig, 'NBA Stats & Covers.com', ax=(ax1, ax2), title=title, subtitle=subtitle,

xoff=(-0.12, 1.01), yoff=(-1.38, -1.45), toff=(-.1, 1.28), soff=(-0.1, 1.08),

prefix = (' ', '$'), suffix=('%', 'k'), suffix_offset=(3, 1), n=80)

plt.show()